Want to know why cloud is the trillion dollar baby

Want to know why cloud is the trillion dollar baby

I've been in the computer business for many decades and I can tell you that the cloud computing market is the most exciting enabler of them.

The next 10 years of cloud will differ dramatically from the past decade, in ways we couldn’t have imagined just a few years ago. I wrote about trillion dollar cloud opportunity in 2015 when I was the first to profile Amazon’s CEO Andy Jassy laying out the first public story about Amazon Web Services (AWS).

The early days of cloud deployed virtualization of standard off-the-shelf components to scale out and build a large distributed system. The coming decade will see a much more data-centric, real-time, intelligent, hyper-decentralized cloud that will comprise on-premises, hybrid, cross-cloud and edge workloads. And it will have a services layer that abstracts away the complexity of the underlying infrastructure.

After decades of cloud innovation, what’s next?

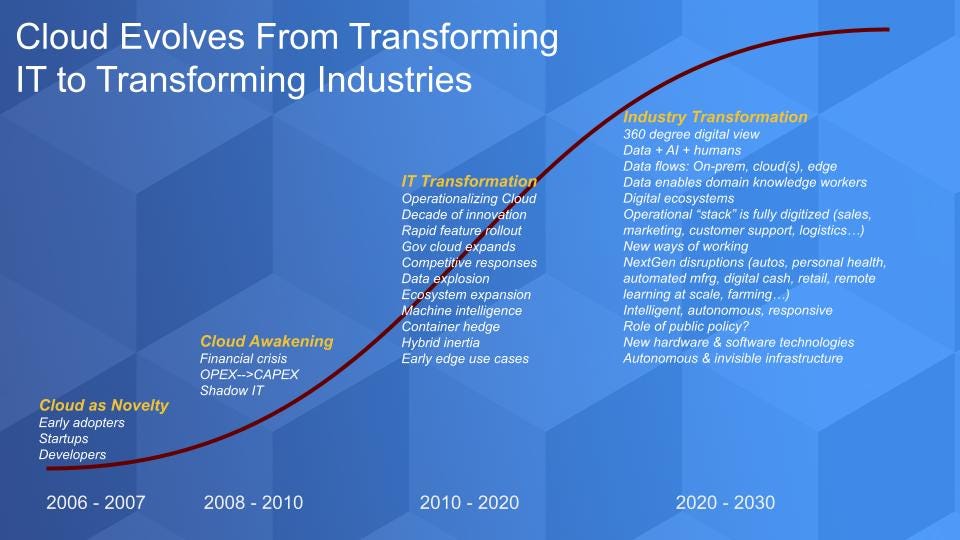

The graphic below lays out our view of the phases of cloud and the progression of innovation over time, and how we see the coming decade.

Cloud as novelty

Cloud, like many innovations, started as a novelty. When Amazon.com Inc. announced S3 in March of 2006, nobody in the vendor and user communities really paid too much attention. Then later that year it announced EC2 and people started to think about a new model of computing. But it was largely tire kickers and bleeding-edge developers that took notice and leaned in.

Cloud awakening

The financial crisis of 2007 to 2009 really created a cloud awakening by putting cloud on the radar of many chief financial officers. Shadow IT emerged within departments that wanted to take information technologies in bite-sized chunks as operating expenses.

A decade of IT transformation

Organizations began to see the benefits of cloud in the form of the agility it brought and cost savings and value creation by re-directing the labor force. It catalyzed the DevOps movement and put developers at the center of IT transformation. Post-financial crisis, we’ve been on an 11-year cloud boom. Cloud has disrupted the on-premises model and completely transformed the way we deploy and manage technology.

Deeper industry transformation is next

The pandemic hit at the beginning of this decade and created a mandate to go digital. And it accelerated this industry transformation that we highlight here, which probably would have taken several more years to mature – but overnight the “forced march to digital” occurred and is here to stay.

This next wave, we think, will be much more about business or industry transformation. We’re seeing the first glimpses of that.

The cloud is the big winner of COVID. Normally we talk about seven-year economic cycles for planning and investment. Now we operate in seven-day cycles. Do we open or close the store? How do pivot to support remote workers, without the burden of CAPEX?

And we think that the focus areas listed on this chart are going to be front and center in the coming years. Data, AI and a fully digitized and intelligent stack will support next-generation disruptions in autos, manufacturing, finance, farming and virtually every industry. The distributed system will expand to the edge and the underlying infrastructure across physical locations will be abstracted. Many issues remain, not the least of which is latency, which we talked about at the event in quite some detail.

The Big 3 clouds: The rich get richer

The chart below shows the most recent estimates of infrastructure-as-a-service and platform-as-a-service spend for the Big 3 cloud vendors.

Combined force of the Big 3: First point we want to make is that combined, the Big 3 — Amazon Web Services Inc., Microsoft Corp. and Google LLC — accounted for almost $80 billion in infrastructure spend last year. That $80 billion annual spend was not all incremental. No — it has caused consolidation in the on-prem data center business. Dell Technologies Inc., EMC, Hewlett Packard Enterprise Co., IBM Corp., Oracle Corp. and others have all felt the the heat and have had to respond with hybrid strategies.

Azure (and GCP) are closing the gap: It’s true that Microsoft Azure and Google Cloud Platform appear to be growing faster than AWS. We don’t know the exact numbers because only AWS provides a clean view of IaaS and PaaS, whereas Microsoft and Google hide the ball on their IaaS numbers because they’re behind AWS. But they do leave breadcrumbs and clues – and we have other means of estimating. But it’s undeniable that Azure is closing the revenue gap with a large revenue base and a growth rate that’s 20 percentage points higher than that of AWS.

AWS continues to lead: However, despite the fact that Azure and Google are growing faster than AWS, AWS is the only company by our estimates to grow its business sequentially last quarter. In and of itself that’s not significant. What is significant is that because AWS is so large at now $45 billion annually, even at slower growth rates it grows much more in absolute terms than its competitors.

We think AWS will keep its lead for some time. We think Microsoft and AWS will continue to lead the rest of the pack; and Google, with its balance sheet and global network, will play the long game. Virtually everyone else, with the exception of perhaps Alibaba, will be secondary participants in this cloud game.

Sizing up the competition

Here are the key points:

Hyperscale leadership: AWS and Microsoft stand alone. They are so far ahead of the pack that they’d have to fall down to lose their lead. They both have high spending velocity and a large share of the market. We don’t think that will change. Google has the financial strength to continue to position itself as an alternative to AWS and as an analytics specialist. So it will continue to grow, but Google will be challenged to catch up to the leaders in our view given the momentum and customer base of both AWS and Azure.

Hybrid cloud becomes real: Now take a look at the hybrid zone – where the whole field is playing. These are companies that have a large on-prem presence and have been forced to initiate a coherent cloud strategy, including multicloud. This includes Google; because it’s behind, it has to take a differentiated approach relative to AWS. And you can see some real progress from the on-prem crowd. VMware Cloud on AWS stands out, as does Red Hat OpenShift, which is “cloudy” although really is not broad IaaS specifically. And there’s VMware cloud, which includes VMware Cloud Foundation, and even Dell’s cloud. We would expect HPE with its GreenLake strategy to pick up the momentum in future quarters.

Captive clouds: And then there’s IBM and Oracle. They are in the game but they don’t have the CAPEX chops to compete with the hyperscale leaders. IBM’s cloud revenue actually dropped 7% last quarter. So that highlights the challenge. Oracle’s cloud business is growing in the single digits and again underscores that these two companies are about migrating their software installed base to their respective captive clouds. As well, IBM, for example, has launched its financial cloud as a way to differentiate and not take AWS head-on in infrastructure.

The bottom line is that other than the Big 3 and Alibaba, the rest of the pack will be plugging into, hybridizing and cross-clouding those platforms. And there are definitely opportunities there, specifically related to creating an abstraction layer that hides the underlying cloud infrastructure — and, importantly, creates incremental value.

My angle: I predict that a new tier of cloud companies will be built on top of current cloud players. Snowflake’s success is the leading indicator that this will happen and happen fast. I call it the “Cloud on Cloud” category.